Component & macro hedging

Component hedging of risk components in non-financial items under IFRS 9. Macro hedging of dynamic banking portfolios under the IAS 39 carve-out and the IASB's evolving DRM model.

Technical advisory and fully outsourced operations across IFRS 9, IAS 39 and ASC 815 — delivered by hedge accountants who have run the function inside corporates and banks, not by generalists with a slide deck.

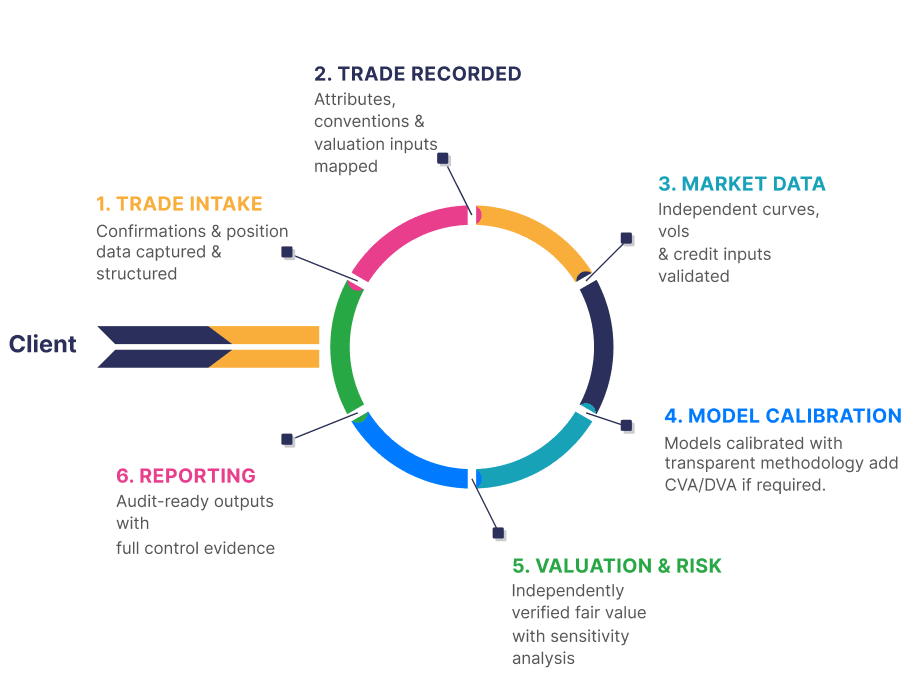

Our workflow

Hedge accounting and derivative valuations sit inside the same engagement. Six controlled steps, from trade intake through to audit-ready reporting — each independently verified and tied to the evidence an auditor or regulator will ask to see.

Need the risk side of the picture as well? Financial risk management sits alongside, covering exposure identification, hedge optimisation and board-level risk framing.

Asset classes covered

Specialisms

The workflow above covers designation, testing, valuation and reporting. These three specialisms sit alongside it for the engagements that need deeper treatment.

Component hedging of risk components in non-financial items under IFRS 9. Macro hedging of dynamic banking portfolios under the IAS 39 carve-out and the IASB's evolving DRM model.

Roadmap from traditional IAS 39 / IFRS 9 hedge accounting to Risk Management Accounting — aligning financial reporting with how the business actually manages risk and reducing P&L volatility.

Counterparty valuation adjustments under ASC 820 and IFRS 13. Expected exposure modelling, collateral effects and disclosure-ready output that integrates with your existing valuation engine.

Standards

Most of our clients report under one and consolidate under the other. We work the boundary in both directions.

Cash flow, fair value and net investment hedges under IFRS 9 for corporates. IAS 39 macro hedging carve-out for banks until the IASB's Dynamic Risk Management model is finalised. IFRS 13 fair value hierarchy and disclosure.

Cash flow, fair value and net investment hedges under ASC 815 with the post-2017 ASU 2017-12 simplifications. ASC 820 fair value framework, Level 1 / 2 / 3 inputs and disclosure for derivative valuations.

Outsourced Operations

Many treasuries do not have, and do not need, a full-time hedge accountant. The work is technical, the volumes are lumpy, and the audit risk is concentrated in a few weeks of the year. Our managed service runs the function end-to-end so the team can focus on the underlying risk decisions.

Everything sits inside your governance — your designation policy, your approved methodology, your sign-off chain. We deliver the production work, the evidence, and the auditor responses; you keep accountability and visibility.

Insights & Brochures

Our technical advisory practice for hedge accounting, financial risk management and regulation.

Guide to transitioning from hedge accounting to Risk Management Accounting under IFRS 9, aligning accounting with economic risk management.

Start a conversation

Book a 30-minute diagnostic call. We'll tell you within the hour whether we can help, and where the biggest wins likely sit.